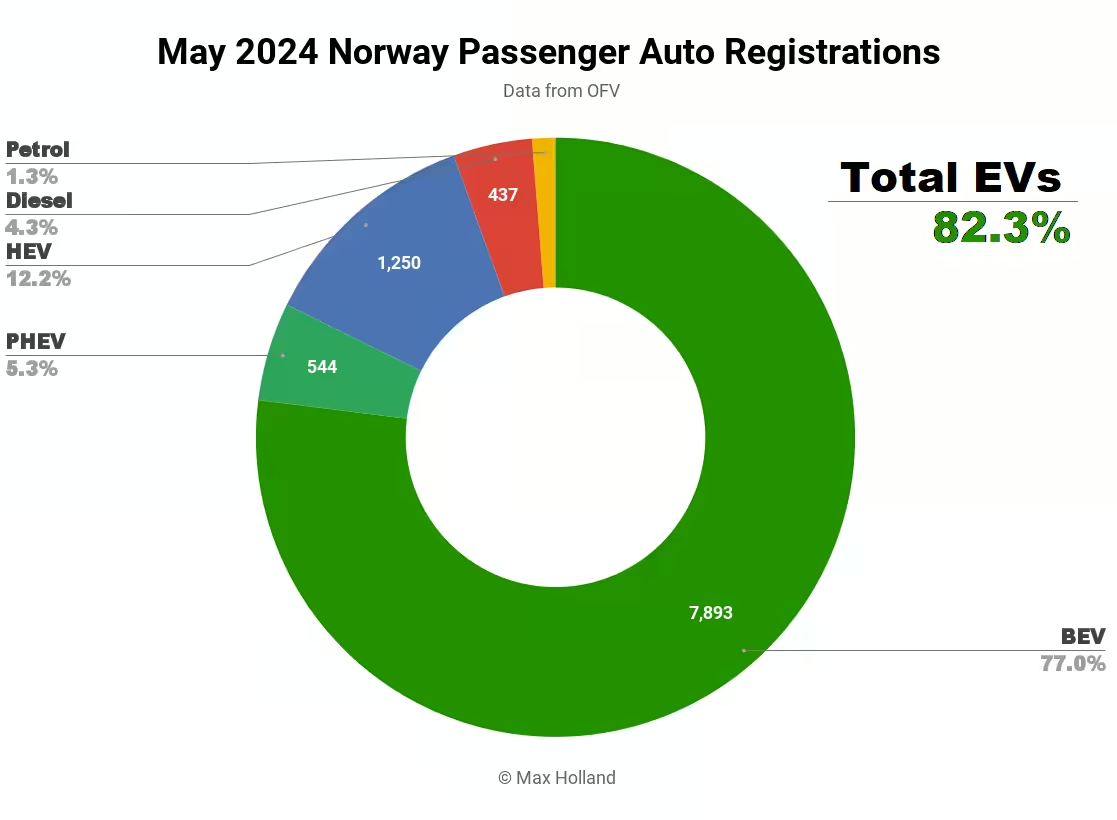

May saw plugin EVs take 82.3% share in Norway’s auto market, down from 88.9% year on year. The dip was likely due to a low ebb of shipping by three of the biggest BEV manufacturers — BEV share is still climbing overall this year. Total monthly auto volume was 7,893 units, down 23% YoY. The new Volvo EX30 remained the best selling auto.

May’s results saw combined EVs take 82.3% share in Norway, comprising 77.0% full electrics (BEVs), and 5.3% plugin hybrids (PHEVs). These compare with YoY figures of 88.9% combined, 80.7% BEV and 8.2% PHEV.

The relatively low BEV volume (and market share) in May is not due to some sudden reversal of buying preferences from the average Norwegian consumer, but instead most likely due to a temporary shipping logistics dip from the three most popular manufacturers. The BEVs from BMW, Volkswagen Group, and Tesla, remain popular in Norway in recent months, though Tesla and VW Group are losing share compared to recent years. Each of these big three brands had a big volume dip in May compared to April, which strongly suggests the influence of erratic shipping allocations, which small markets (like Norway) can suffer from.

Volkswagen Group BEVs saw 1,895 registrations in May 2024, 805 units down from May 2023. In April, however, the group registered 3,173 units, which was 703 units up on April 2023. Likewise BMW saw 303 registrations in May, down 538 from May 2023. April 2024, however, saw 576 units, up by 85 units YoY.

Tesla saw 830 registrations in May, down by 2116 units YoY. In April, however, their volume was 872 units, just 10% off YoY.

In sum, these three manufacturers saw a shortfall of 3,459 deliveries in May, whereas BEVs overall were 2,880 units down. Put differently, excluding these big three, sales of BEVs from all other brands actually increased by 14%, or around 580 units YoY. Much of this growth came from the Volvo and MG brands, with other brands fairly flat YoY.

Long story short – BEVs likely don’t have any significant demand-side problem in Norway — beyond the broader economic slowdown — as they are as popular as ever so far this year in terms of market share. However, small volume markets are vulnerable to the vagaries of batch shipments and erratic temporary allocation priorities, in other words, supply-side challenges.

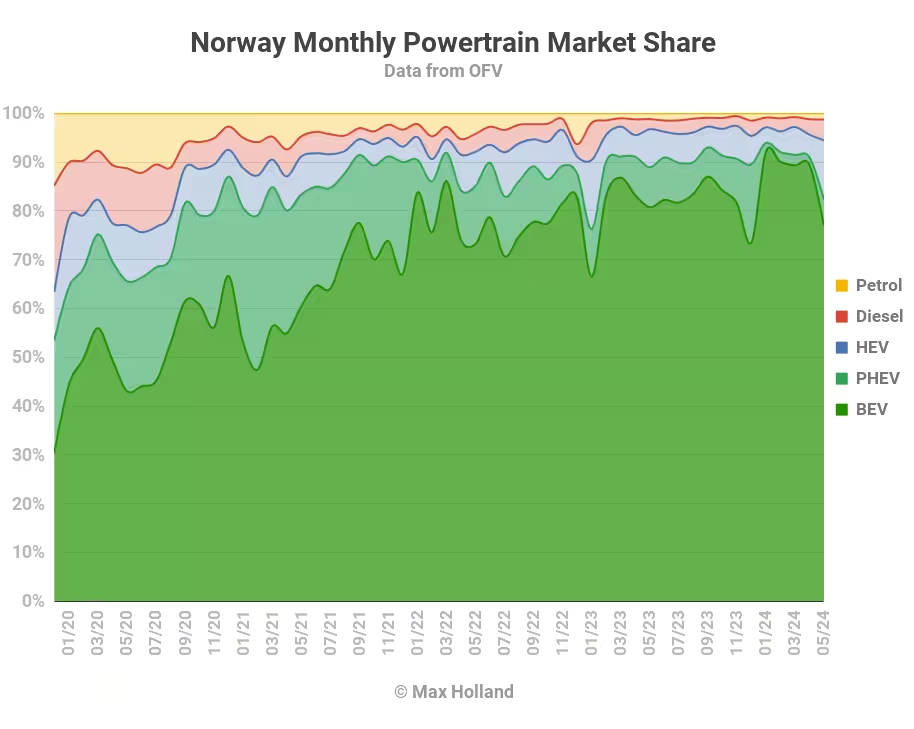

With BEVs at temporary low volume, other powertrain shares looked relatively shiny in May. For some reason (ask Toyota), May is one of the year’s peak months for plugless HEV sales, so HEV share temporarily looked good at 12.2%. Stepping back, year to date HEV volume is down 15% from the same period in 2023, and their overall share has fallen, currently at 6.4%.

Petrol-only sales are down by 24% year to date, and diesel-only sales are mostly flat (up by 31 units YTD). Combined, combustion-only sales continue to fall, but stubbornly cling on to around 4% of the market. This will likely only diminish towards near-zero when a broader selection of compelling BEVs are available, and price competitive, across all auto market segments.

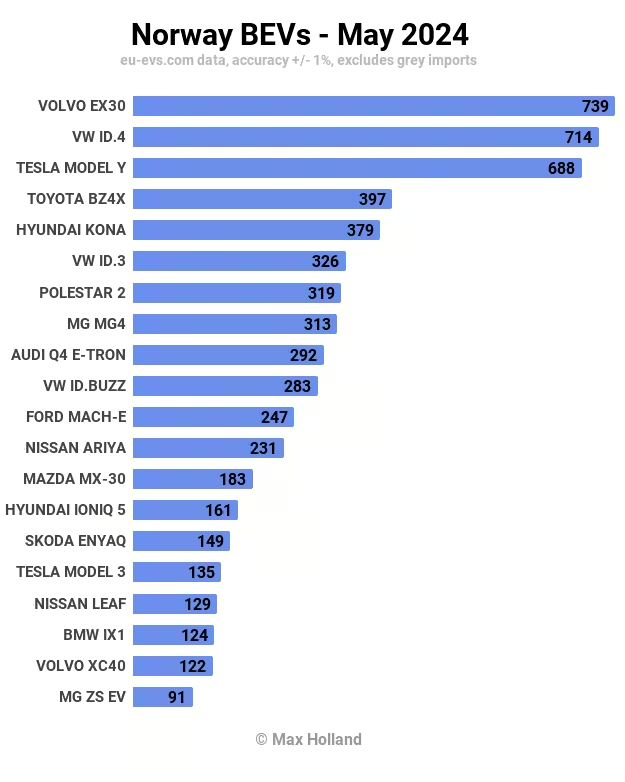

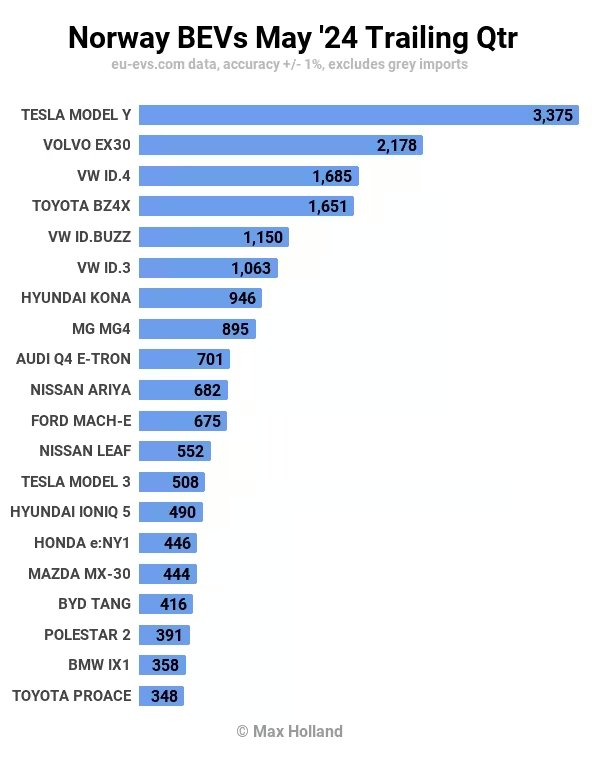

Most Popular BEV Models

The best selling auto in May was once again the new Volvo EX30, with 739 units, its second month in the top spot. In number two spot was the Volkswagen ID.4, with 714 units.

The Tesla Model Y came in third, with 688 units, though it retains the 3-month top spot.

There were no dramatic changes in May’s top 20, except for the return of the long-lost Polestar 2 to the upper ranks, after a long period of low volumes. For context, its recent two-month total, starting in April and more strongly in May, summed to more units than delivered over the previous 15 months combined!

I don’t have insights into Polestar’s market strategy in Norway, and why they went slow from January 2023 until March 2024, please jump into the comments if you have a clear perspective on this.

In terms of new BEV models, there were two notable debuts in May. The new Renault Scenic delivered 40 initial units. This is a 4,470 mm long CUV / MPV, sharing a platform with the Renault Megane, and Nissan Ariya. For more details, see my recent Sweden report, since it has also just debuted in that neighbouring country.

The other debutant was the BYD Seal U SUV, which registered an initial 20 units. This is a bigger vehicle. with length of 4,785 mm, a competitor of the Tesla Model Y, though somewhat less expensive. For more details, again, see the Sweden report.

There were 2 units of the Polestar 3 registered in May, but these may be dealer-only examples for now, let’s look for customer volumes to appear before we look at this model in more detail.

Models we first saw released in April, the Peugeot e-3008, and the KGM Torres, both saw a ramp in volume in May, to 58, and 28 units, respectively.

Let’s now check up on the 3-month picture:

We can see the Tesla Model Y’s lead is still strong, although the Volvo EX30 may be able to get closer later this year. June’s expected Tesla push will likely extend the Model Y’s lead for the coming few months.

While it is generally true that Tesla and Volkswagen Group BEVs have not kept the oversized share of the Norwegian market that they had a year or two ago, they still remain by far the strongest in sales for now.

The issue they face right now is that neither have been pushing the market forward with simple and affordable models in recent years. The Model 3, and the ID.3 did break new ground on affordability when they were launched, but that was 7 and 4 years ago, respectively.

The costs of BEV batteries and powertrains have reduced substantially since then… and other brands are now offering much more affordable models (see positions #2 and #8 in the above ranking).

For a fleet transition update, see last month’s Norway report.

Outlook

Year to date, the auto market is down by 14% from last year. This reflects the negative turn of the broader Norwegian economy, whilst interest rates remain high. Q1 2024 (latest data) saw economic output at negative 0.8% year on year, from +0.3% in Q4, and -2.0% in Q3. Meanwhile, inflation is at 3.6% and interest rates remain high at 4.5%. Manufacturing PMI in May was 52.3 points, a slight downturn from 52.6 in April.

The OFV said in their April report that “People have a more strained economy… We now show greater moderation and buy smaller and more affordable new cars… We will probably have to wait until the first interest rate cut before optimism returns to new car buyers” (OFV April statement, machine translated).

These factors remained in play in May, and likely will continue for most of this year.

What are your thoughts on Norway’s transition to EVs? Please jump in below and join the conversation.