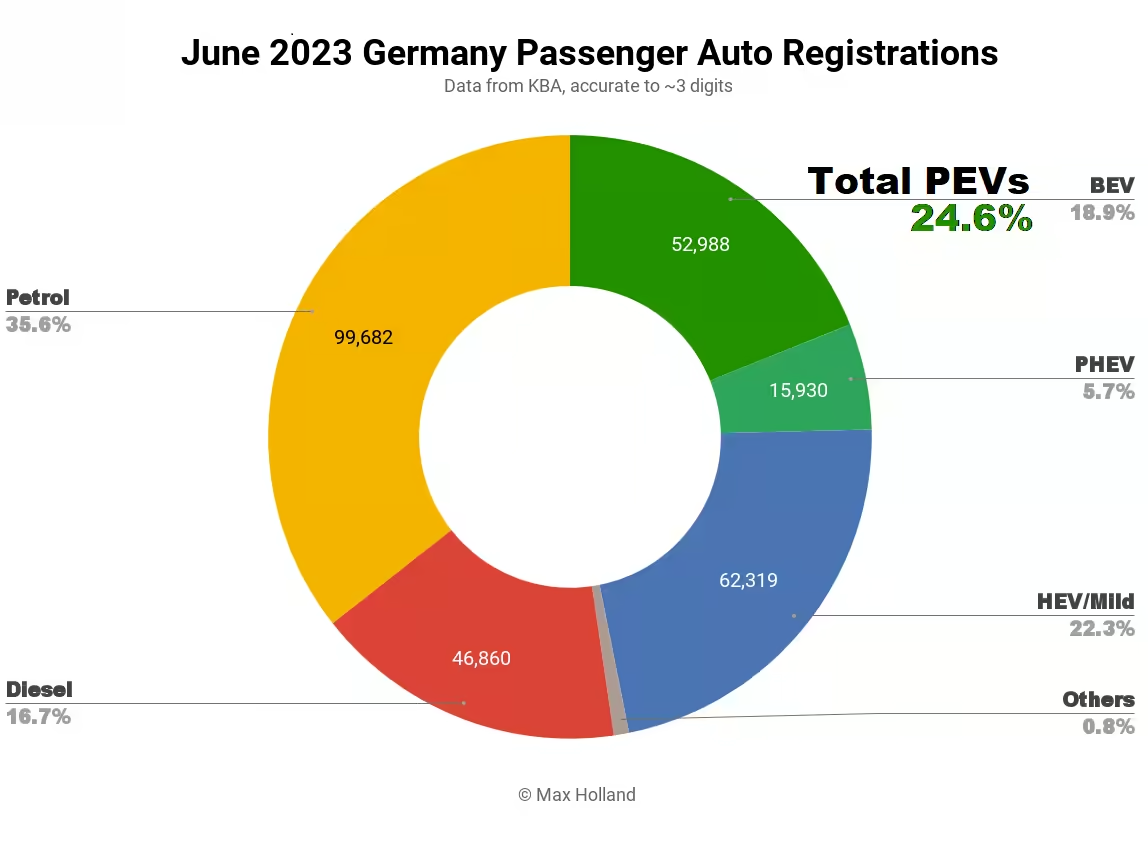

June saw plugin EVs at 24.6% share in Germany, down from 26.0% year on year. Full electrics grew their share at a decent rate, up from 14.4% to 18.9%, the share of plugin hybrids halved, however, after incentives were cut. Overall auto volume was 280,047 units, up 24.7% YoY, still far down on the pre-2020 norm (roughly 330,000). The Tesla Model Y was the best selling BEV in June, and third best seller of any auto.

With combined plugin EVs at 24.6% share in June, full electrics (BEVs) contributed 18.9%, and plugin hybrids (PHEVs) contributed 5.7%. These compare with like figures of 26.0%, 14.4%, and 11.7%, a year ago.

Recall that Germany entirely cut the ecobonus for PHEVs from January 1st this year, and their fall in share since then was fully expected. Their decent 11.2% share of the market in H1 2022 has halved, to 5.66% in H1 2023.

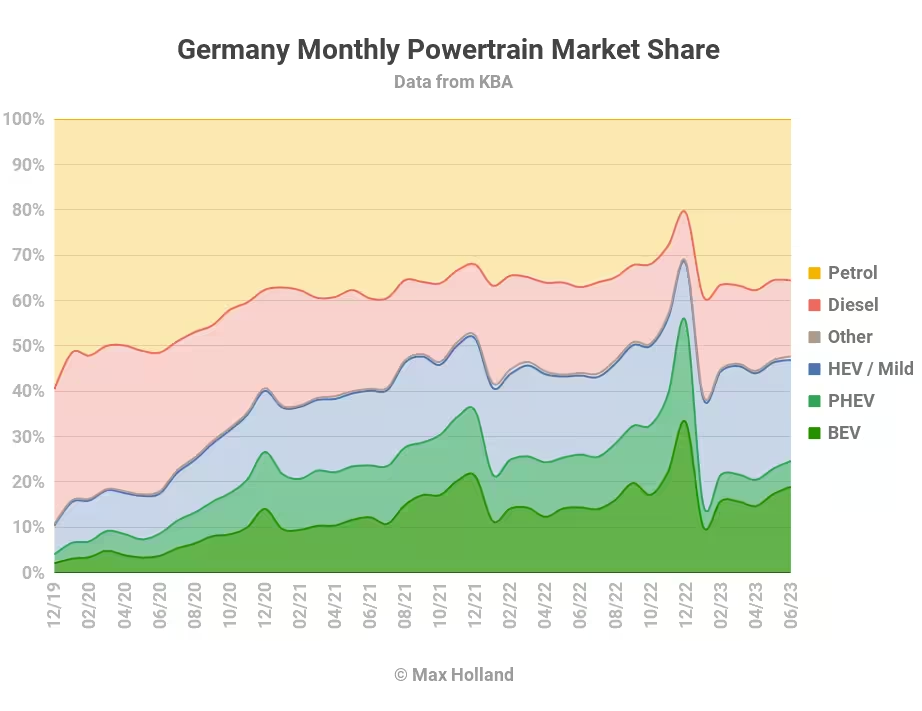

BEVs also took a moderate trim to their incentives from January 1st, which led to relatively slow sales at the start of this year. Q1 volume growth for BEVs was just 13.2%.

As time goes on, and the memory of the “good old days” of more generous incentives fades, BEVs have returned close to their usual growth trajectory. Q2 volume growth was 50.1%.

Whereas PHEVs previously had almost as much market share as BEVs (see graph below) in Germany, they have now slipped to around one third that of BEVs. This is more in line with the plugin weightings in the other large European markets of France and the UK.

Unfortunately, these temporary Eddie-currents and adjustments mean that Q1 didn’t see the share of combustion-only vehicles shrinking at all. The past two months of May and June have shown signs of returning to trend however.

As the plugin market continues to settle down in the coming months, we can fully expect the recent patterns of the EV transition will resume. Over 50% YoY BEV volume growth in Q2 sends a strong signal.

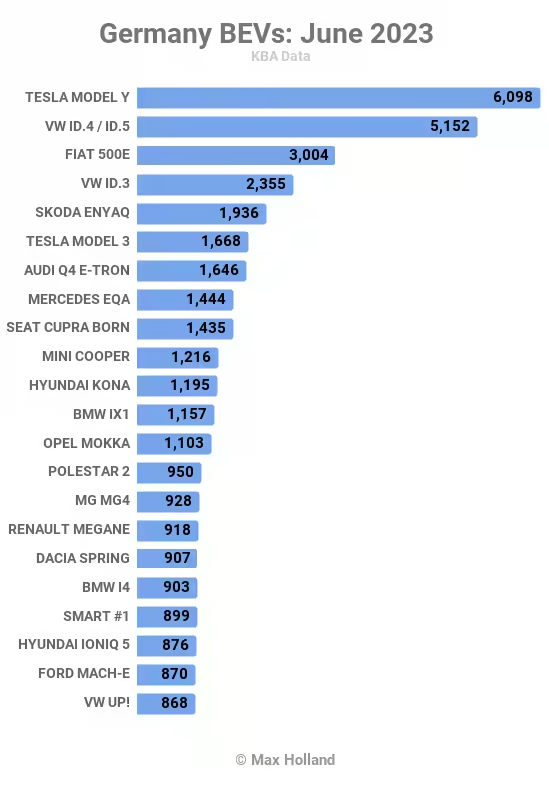

Best selling BEVs in June

The Tesla Model Y was the best selling BEV in June (6,098 units), and third best selling of any vehicle in Germany. Only the Volkswagen Golf (7,019 units) and Tiguan (6,329) sold more.

Most of the Model Y units are now coming from local production in Berlin-Brandenburg. We know that weekly production passed 4,000 units in late March, and is presumably closer to 5,000 units by now. Tesla will likely give a capacity update in their Q2 results discussion on July 19th.

Not far behind Tesla in the June BEV rankings were the Volkswagen ID.4/ID.5 in second place, and with the Fiat 500 a long way back in third.

This is the best monthly performance YTD from the Fiat 500, 70% higher volume than its recent average, reclaiming the kinds of performance that it was achieving in Germany throughout much of 2022.

Further down, in 13th place, the Opel Mokka is experiencing its own similar renaissance (volume 69% above recent averages). This has been helped by the spring refresh which has effectively given it a very welcome 20% boost to range.

Other relatively strong performances were shown by the Renault Megane, the Dacia Spring, and the Smart “#1”. The Smart saw its highest ever monthly volumes at 899 units, not far off doubling its previous high just last month.

In terms of newcomers, the Aiways U5 made its German debut in June, albeit with a modest 15 initial units. It may just be testing the waters for now, as its sibling, the U6, did a few months ago.

The new Honda “e:Ny1” (let us know what you think of this name in the comments) also made its debut, with just 5 units. This is Honda’s first all-round competent BEV (412 km WLTP rating), though with fairly weak charging speed (46 minutes 10% to 80%), with low peak. Perhaps Honda is being initially cautious until it has some data, and may unlock higher power charging later, as some other BEV brands have done. Its starting price is around €48,000. Presumably any Honda loyalists that may exist in Germany will want to check it out, but it will not attract large interest unless more charging power is unlocked.

The Lucid Air made its first volume deliveries, with 33 units in June (from just one or two scattered units previously). The new Opel Astra also saw its first decent volume, with 215 units (up from previous high of 42 units in March). The Nio ET7 saw a similar step up, though to a more modest 99 units in June.

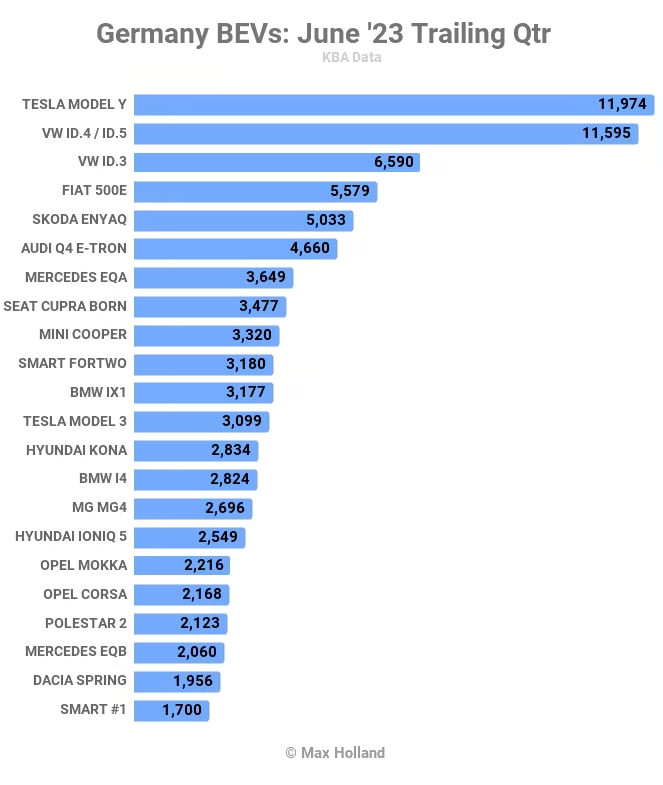

Let’s now turn to the 3-month perspective:

In Q2, the race between the Tesla Model Y and Volkswagen ID.4/ID.5 was very close, and both were well ahead of other BEVs. The Tesla was in fact 24% down in volume over Q1, presumably due to some country supply shuffling. The Volkswagen was 71% up in volume over Q1.

The significant climbers in the top 20 were the Mercedes EQA (up 7 spots to #7), the BMW iX1 (up 7 spots to #11), and the BMW i4 (up 11 spots to #14). Let’s see if the premium local brands can maintain these volumes of their most affordable BEVs.

Let’s also give a shout out to the Opel siblings, the Mokka and Corsa, which — thanks to the upgraded battery and efficiency — are both now in the 400+ km club for rated range. Both have climbed 9 spots back into the top 20.

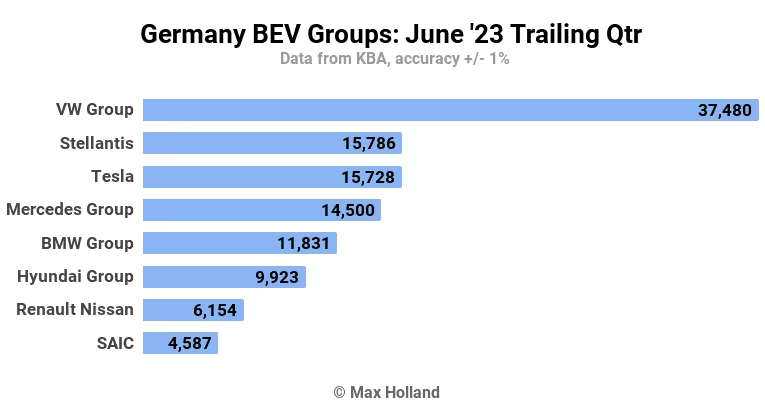

Now we can have a quick look at manufacturing group performance:

Over the past 3 months Volkswagen Group’s lead has extended. It previously had around 29% of the BEV market, and now has 30%.

Tesla has fallen from 2nd to 3rd, dropping from 22% share to just under 13% share, as its volume dropped by 24%. That was a relative tumble in a BEV market that grew by 33% over the period. Tesla’s volume dip is likely a result of regional allocation shuffling rather than any inherent lack of demand for Tesla in Germany. Tesla’s Europe-wide share hasn’t changed much this year.

Stellantis has seen remarkable growth recently in Germany stepping up from 4th into 2nd place, and from 8.6% share to almost 13% share, with 95% volume growth from Q1 to Q2.

Mercedes dropped down a spot from 3rd to 4th, though its share increased fractionally, now at around 11.7%. Its volume growth was just ahead of the overall market, at almost 36%.

The other positions were largely unchanged.

Outlook

Germany’s economy is not in a good place, with GDP contracting by 0.5% in Q1 2023, the worst performance since the 2008 financial crisis (putting aside Covid disruptions). A big part of the problem is high inflation — affecting energy prices for industry, and all prices for consumers — as well as high interest rates. Inflation was at 6.4% in June, up from 6.1% in May.

As for general business confidence, the latest IFO survey for June finds the lowest rates since December. Confidence was down from May, both in terms of current assessments, and in future expectations.

Specific to the German auto industry (the country’s largest employer), IFO finds that auto manufacturers’ assessment of their current situation improved over May, though automotive suppliers’ assessment was down from May. As a whole, the auto industry’s future expectations bleakened, falling for the fifth month in a row, coming close to 2008 levels.

To attempt to balance the books, auto makers are looking to raise prices, IFO director Oliver Falck reports, “these price increases will mainly affect the premium segment and electric vehicles”.

Sometimes in the comments we find the idea that a weak German auto industry is somehow “a good thing” for the EV transition, whatever the impact on the welfare of working families. Even by its own twisted logic, the increased pricing of electric vehicles shows this to be a false perspective. Change needs investment, and investment is nurtured by conditions of economic stability and predictability.

What are your thoughts on the German auto market’s transition to EVs? Jump in to the conversation in the comments below.