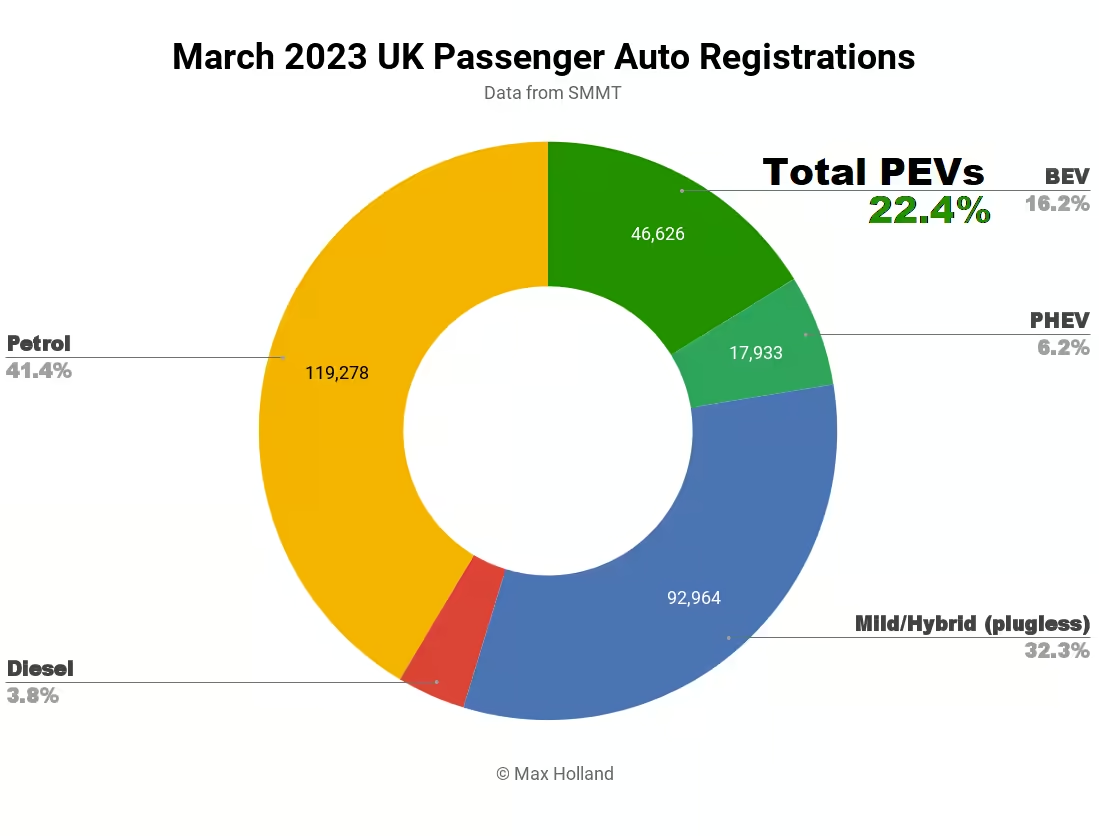

The UK saw plugin electric vehicles take 22.4% of the auto market in March, down from 22.7% year on year. BEVs saw fractional market share growth YoY, and a new volume record, whilst PHEVs saw a slight decline. Combustion-only powertrains lost 2.5% share YoY. Overall auto volume was 287,825 units, up some 18% YoY, though still some 19% down from March 2019 levels. The Tesla Model Y was the UK’s overall best selling auto in March.

March’s combined plugin share of 22.4% comprised 16.2% full electrics (BEVs), and 6.2% plugin hybrids (PHEVs). These shares compare with YoY figures of 22.7%, 16.1%, and 6.6%.

In terms of volumes, against a backdrop of 18.2% overall auto sales growth YoY, BEVs stayed just ahead of the broader market, with 18.6% growth (to 46,626 units). This was a new record for BEV volume in the UK (from 42,284 in December ’22). PHEVs slackened, with just 11.8% growth (to 17,933 units), thus denting the overall plugin share, YoY.

Hybrids (HEVs) and mild hybrids continued to see strong growth in the UK, with 32.3% combined share of the overall market (from 29.6% YoY). This category, however, is a temporary transition technology away from combustion-only, but will itself give way to plugins, and eventually to almost entirely BEVs. HEVs and mild-hybrids are offered by manufacturers as a quick and relatively cheap way (especially in the case of mild hybrids) to improve fleet emissions, compared to ICE-only vehicles.

HEVs can save around 25% fuel use over ICE-only, whereas for mild hybrids, the figure is around 10% to 15% (EPA estimates, depends heavily on typical driving cycle). Whilst these are welcome improvements over ICE-only — especially when introduced in 1997 — they are not the final answer in a world where compelling BEVs now exist, and their technology and affordability is rapidly improving, along with densifying charging networks.

Diesels continued to slide, taking just 3.8% of the market (only December ’22 was lower), from 5.6% YoY. Their trajectory in the chart below suggests that they may dwindle to around 1% by 2025. This is roughly where they are in Norway today.

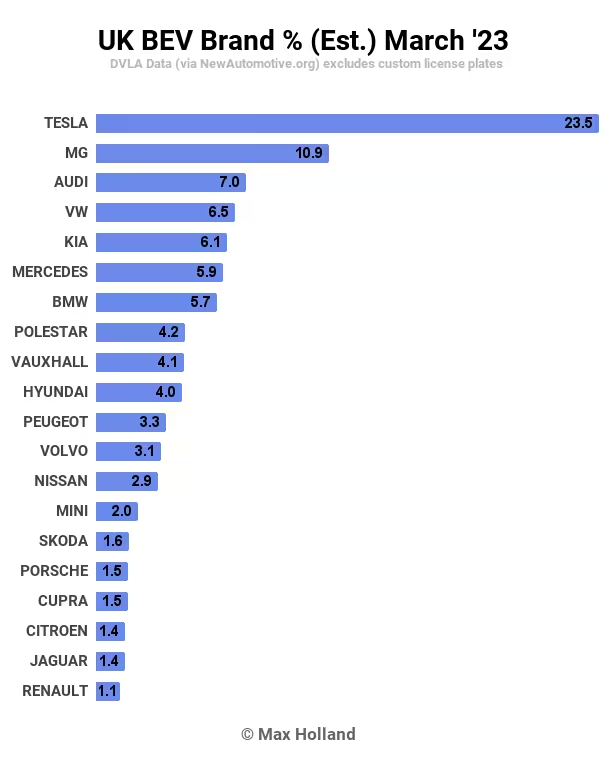

Leading BEV brands

Tesla had yet another knock-out performance from the Model Y in the UK in March. It was the UK’s best selling vehicle (of any kind) for the month, with 8,123 units registered (just below its December all-time record).

For the Model Y, this represented a 26% YoY volume boost. However, Model 3 shrank sales YoY, such that combined Tesla volumes were down. Likely this was less to do with demand softening, and more to do with the variable logistics of producing and supplying batches of right-hand drive variants for the UK market.

Second placed brand was MG, now offering 3 great value BEVs in the UK market (when will the Marvel R join them?), of which the MG4 was the second best seller after the Model Y. Audi rounded out the top three spots.

In terms of movements in rank, MG’s climb to 2nd spot came off the back of a slow February, when it was only in 17th place. Again, this change results from logistics shuffling, rather than reflecting any abrupt demand fluctuations. March appears to have been the brand’s highest ever BEV volume in the UK market (over 4,000 units).

Outside the top 20, BYD made its first measurable deliveries of the Atto 3 (approximately 34 units). Being a similar size and shape to the very popular Kia Niro, the Atto 3 has every chance of eventual success in the UK market.

Stellantis brands, having had a slow January and February, returned to better form in March, with Citroën especially returning to volumes not seen since Spring 2022 (over 500 units), almost all of them the e-C4 compact SUV.

It will be interesting to see the popularity of the Stellantis’ incoming Opel (Vauxhall) Astra, and platform-sibling Peugeot e-308, in the UK market. These are expected to start to arrive from June onwards. Stellantis are one of the few legacy auto groups which have been offering “relatively” affordable BEVs, but whose WLTP range up until now has been a bit modest for some consumers.

The Astra and e-308 will finally offer a somewhat larger battery with WLTP range of over 250 miles (> 400 km). This larger battery will then later make its way into updated versions of the existing Stellantis BEVs (e-208, Corsa-e, e-C4, etc).

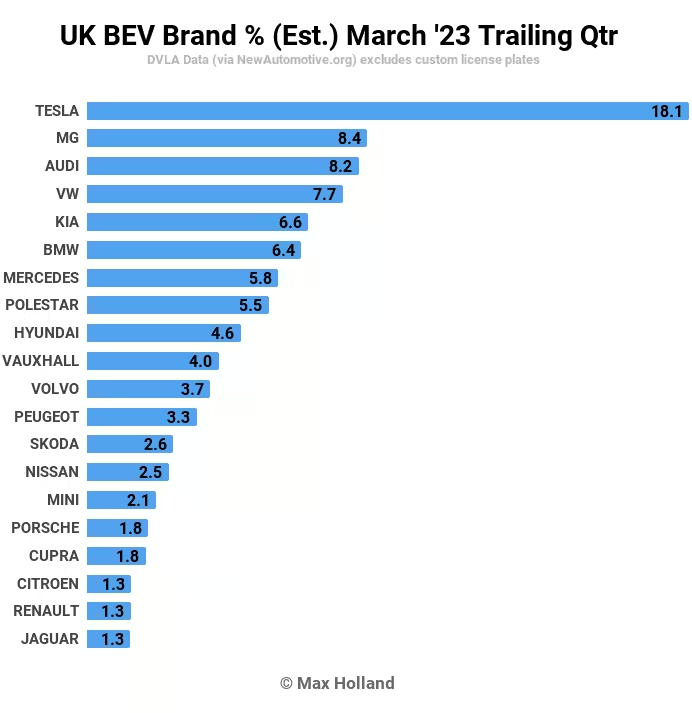

Let’s now review the trailing 3-month brand charts:

Here Tesla remains firmly in the lead, taking over 18% of the UK BEV market in Q1. The remaining ranks are more closely distributed, with MG and Audi in 2nd and 3rd spots.

In terms of the changes since Q4 2022, Tesla has kept its lead, though its market share shrank from the previous 25.5%. Here are the main gainers compared to Q4:

- MG up from 4th to 2nd

- Audi up from 6th to 3th

- Kia up from 14th to 5th

- Peugeot up from 16th to 12th

- Citroen up from 21st to 18th

On the flip side, these brands slid since Q4:

- BMW down from 2nd to 6th

- Nissan down from 5th to 14th

- Renault down from 9th to 19th

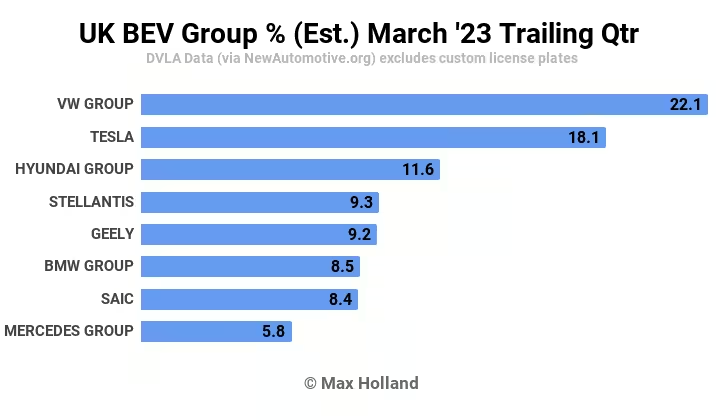

Let’s now briefly review the manufacturing group performance in Q1:

Here Volkswagen Group and Tesla swapped places compared to Q4, with the former gaining 2% share, and the latter losing 7%.

Hyundai climbed from 6th to 3rd, and Stellantis climbed from 8th to 4th. Geely stayed in place in 5th, as did SAIC in 7th. BMW, however, slid from 3rd in Q4, to 6th in Q1.

Renault-Nissan had the biggest drop, from 4th in Q4 (with 9.3% share), to 9th in Q1 (3.8% share).

Outlook

The UK economy continues in the doldrums, with forecasters split over whether it will show mild recession this year, or simply zero growth. The latest inflation rate figures show a slight rise to 10.4%, though business confidence has somewhat improved recently.

The auto industry body, the SMMT, is forecasting the auto market to be one of the few prospective growth stories of the coming year. CEO Mike Hawes said: “With eight consecutive months of growth, the automotive industry is recovering, bucking wider trends and supporting economic growth. The best [volume] month ever for zero emission vehicles is reflective of increased consumer choice and improved availability but if EV market ambitions – and regulation – are to be met, infrastructure investment must catch up.”

For owners who can access time-of-use electricity tariffs, especially cheaper overnight rates when plugged in at home, BEVs still have much lower total cost of ownership than ICE vehicles. We can thus expect demand for them to continue to steadily climb over time — their actual rate of market share growth will likely be more constrained by supply than demand.

What are your thoughts on the UK’s transition to electric vehicles? Jump in below to join the discussion.